1. Introduction: The Down Payment Hurdle

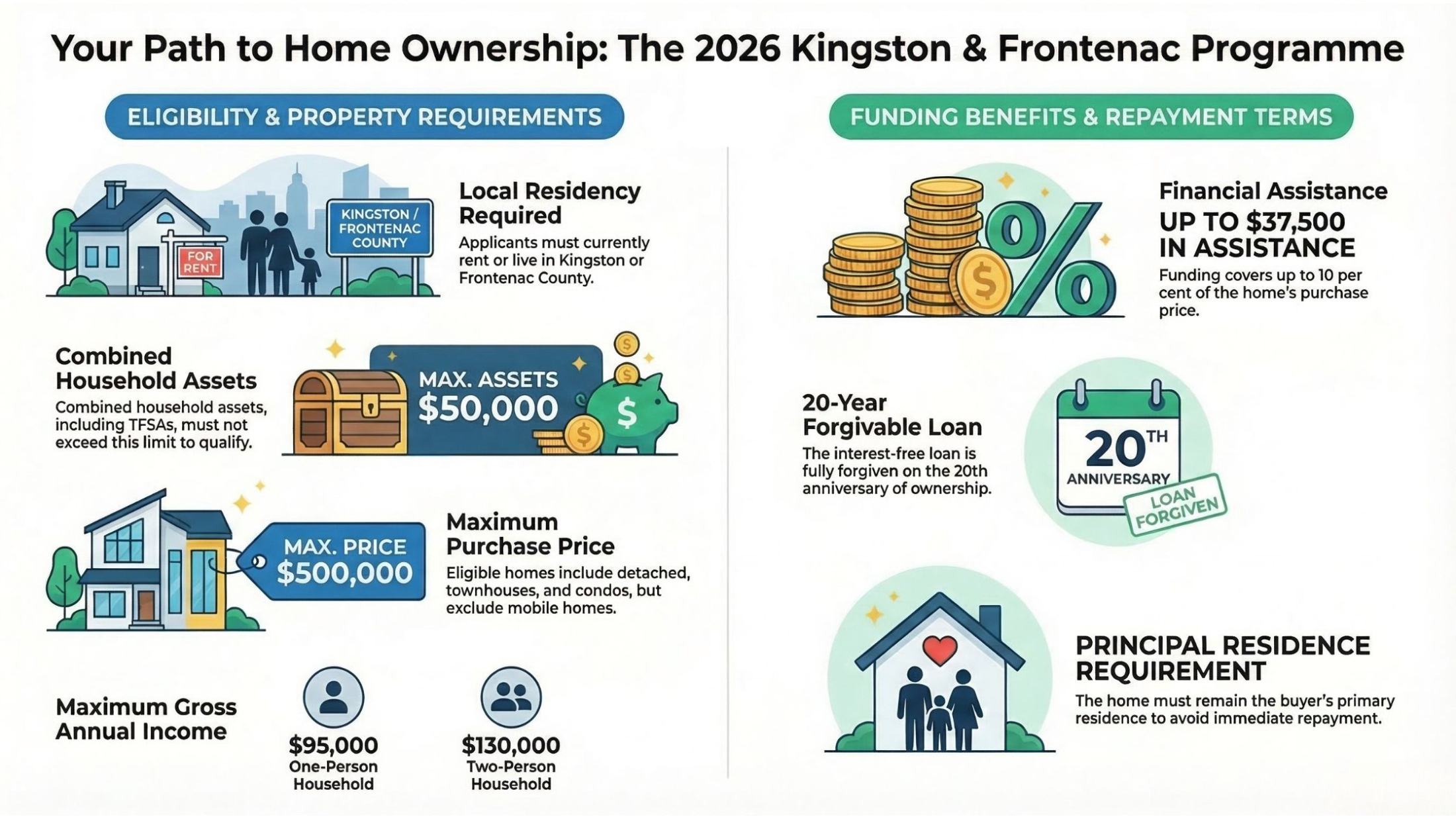

In the current real estate climate, the "rent trap" is a reality for many hardworking residents of Kingston and Frontenac County. The challenge isn't usually the ability to carry a monthly mortgage; it’s the monumental task of saving a five-figure down payment while simultaneously battling rising rental costs. As a real estate agent, I’ve seen many potential buyers sidelined simply because they lack that initial capital injection.

The 2026 Kingston and Frontenac Home Ownership Program is the transformative solution we’ve been waiting for. This isn't just a grant; it’s a strategic "leg up" designed to move you from the sidelines into your own front door. By dismantling the down payment barrier, the City is providing a path to equity that would otherwise take years—or even decades—of disciplined saving to achieve.

2. Takeaway 1: A Substantial Financial Head Start

The core of this program is a powerful boost to your purchasing power. By providing a significant portion of your down payment, the program increases your leverage with lenders and can substantially lower your monthly carrying costs by reducing your total mortgage principal.

"The maximum funding is 10 per cent of the home's purchase price, up to $37,500."

From a strategist's perspective, $37,500 is more than just cash—it’s a way to potentially avoid high-ratio mortgage insurance premiums or to qualify for a more stable home that fits your long-term needs. This funding allows you to enter the market sooner, capturing appreciation early rather than chasing a moving target.

3. Takeaway 2: The 20-Year Path to Forgiveness

The structure of this assistance is unique and requires a long-term mindset. It is not a gift, but an investment in your residency within our community.

"It is a 20-year interest-free forgivable loan registered on the property's title."

Strategic Insight: You must view the City as an equity partner. If you remain in the home as your principal residence for the full 20 years, the loan is forgiven entirely—a 100% gain for you. However, if you sell or move out before that 20th anniversary, the "gotcha" applies: you must repay the original loan plus 10% of any capital appreciation. Essentially, if your home’s value grows, the City shares in that profit. The winning strategy here is clear: buy a home you can see yourself in for two decades to keep every cent of that equity for yourself.

4. Takeaway 3: Broad Eligibility with Strict Guardrails

The program is designed for modern, middle-income households, but the criteria are rigid. I must highlight that this program is strictly for those who can qualify for a mortgage on their own merit.

Residency & Status: You must currently live in Kingston or Frontenac County and be a Canadian Citizen or Permanent Resident.

First-Time Buyer: You cannot currently own property or have participated in this program previously.

Income Caps: Gross household income is capped at $95,000 for one-person households and $130,000 for two-person households.

Asset Limit: Your combined assets must not exceed $50,000.

Strategic Warning: The Co-Signer Ban

One of the most critical "deal-breakers" in the guidelines is that applications supported by a co-signer or guarantor are ineligible. You must be able to secure a mortgage pre-approval from an approved lender (bank, credit union, or MIC) based solely on the income of the residents who will live in the home. Additionally, be aware that while RRSPs and RESPs are exempt, funds in TFSAs and FHSAs are included in your $50,000 asset limit.

5. Takeaway 4: Flexibility and Its Limits

The program covers a wide range of lifestyles, with a maximum purchase price of $500,000. Eligible units include detached homes, semis, townhouses, and condominiums. However, there are several exclusions and requirements you must plan for:

Ineligible Properties: Mobile homes and multi-residential properties do not qualify.

The Inspection Rule: For all resale homes, a professional home inspection is mandatory, and you must provide the report to the City.

Program Exclusions: This funding cannot be combined with the Kingston-Frontenac Renovates Program.

Pro Tip: Do Not Sign Prematurely

Applicants who make an official offer on a property before receiving written application approval are automatically disqualified. You must have your Letter of Conditional Approval in hand before you sign an Agreement of Purchase and Sale.

6. Takeaway 5: The "First-Come, First-Served" Clock

This is a high-stakes race. Funding is limited, and the clock starts on Wednesday, April 1, 2026, at 8:30 a.m.

The most important strategic advice I can give is this: An incomplete application is a wasted application. You will not secure a spot in line until every piece of documentation is submitted. Use the time leading up to April to gather your "Submission Ready" folder:

Proof of Status: Birth certificates or Passports for all owners.

Tax Records: 2024 or 2025 Notices of Assessment (NOA) for all adults.

Bank Statements: The two most recent months for all accounts (including TFSA/FHSA).

Mortgage Pre-Approval: A signed letter from an approved lender (no private/unregulated lenders).

"Approved applicants... have 90 days to provide a purchase agreement; the closing date of the purchase may be beyond the 90 day date."

Once you are approved, you have a 90-day window to find your home. If you miss this window, the funding commitment is withdrawn.

7. Conclusion: Moving Toward Your Future

The 2026 Home Ownership Program is a rare opportunity to bypass the hardest part of the home-buying process. By staying the full 20 years, you aren't just securing a roof over your head; you are executing a financial strategy that builds significant wealth for your future.

As you prepare for the April 1st deadline, ask yourself: Where could you be by the 20th anniversary of your first home? With $37,500 in assistance and a clear-eyed strategy, that future is closer than you think.

Ready to start? We can help!

Visit the City of Kingston website to learn more

Contact us and we will connect you with a lender so that you can start your pre-approval

Let’s meet for a buyer consultation - this will prepare you to search and find a home that meets all the program criteria